Who is this for:

The Acquire Then Retire retirement savings challenge is for those who want to retire comfortably with millions in the bank. It’s also for folks that want to be able to enjoy life both now and in old age. This challenge works best for people who have a retirement plan offered by their employer, but can be applied to an IRA or Roth IRA.

Are you ready to retire comfortably without sacrificing your quality of life? You can sign-up for Acquire Then Retire on the Ostrich app.

Traditional 401(k)/403(b) Example:

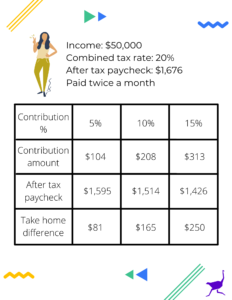

Let’s say you make $50,000 before taxes and have a traditional (non-roth) 401(k)/403(b).

You decide to set your 401(k)/403(b) contribution to 10%.

Assuming you get paid twice a month, that would be contributing $208 each pay period. But you only would see your after tax pay (what’s in your paycheck) go down by $165.

The difference is an extra $43 you keep simply by paying yourself first in your retirement account.

The reason this happens is because you are contributing money to your retirement savings before taxes. This lowers the amount of money you make that is taxable.

Pretty neat huh?

So bumping up your contribution percentage to 11% would be $229 contributed to your retirement account. Yet, only $172 would come out of your take home pay, a difference of $16 from the 10%.

Don’t you like keeping more money just by directing it to your retirement account instead of your checking account?

So each month bump it up 1% point until you hit a comfortable level where you aren’t struggling to pay for your basic necessities.

As you grow in your job and receive pay increases the dollar amount you contribute will increase and your take home pay will grow as well. You’ll be paying yourself first and future you will be grateful.

It’s usually a good idea to reassess your contribution percentage when you receive a raise. Frequently, salary increases don’t come with expense increases in equal amounts! Bumping up your retirement contributions is a great use of those extra leftover dollars each month.

The ultimate goal is to max out your retirement accounts every year. You can find the current contribution limit on the IRS website: 401(k), 403(b), IRA.

Roth 401(k)/403(b) Example:

For those of you with a Roth 401(k)/403(b) then the numbers will look a little different. You’ll be contributing after-tax dollars so your paycheck will be reduced by the actual dollar amount you contribute. But all of your withdrawals from your Roth 401(k)/403(b) will be tax free assuming you wait until retirement to access the funds.

This can be a huge advantage, given the likely growth that your invested retirement funds will experience during your career. Check out our Retirement Investing 101 Guide for a demonstration of the potential numerical advantage of Roth accounts over Traditional.

How to implement the Acquire Then Retire retirement savings challenge

Step 1

Sign-up for this challenge on Ostrich and then login to your 401(k)/403(b) account or whichever work provided retirement account you prefer.

Step 2

Find where it lists your contribution percentage. Bump it up a percentage point (or 2).

BONUS

If your employer offers a retirement matching program, ensure that you are contributing at least the percentage your company matches up to. Otherwise you are leaving free money on the table.

Step 3

Confirm the new amount.

NOTE: It can take 2 pay periods before your new contribution percent takes effect.

Step 4

If you didn’t miss that little bit of money, repeat these steps until you hit a comfortable level.

Step 5

Check-in on Ostrich each month and grow your wealth with The Flock!

Tools to get their quicker

Retirement Account

Don’t have a work retirement account? That’s okay! Setup an individual retirement account (IRA) that you control through one of our partners.

Employer Match

It is worth repeating. If your company offers a retirement matching program, you should at a minimum contribute this amount. Otherwise, you are leaving free money on the table.

Commission or bonus-based jobs

If you earn a commission or bonus on top of your base salary, your employer may allow you to have different contribution percentages for each. In that case, try doubling or raising your bonus or commission checks to an even higher level. If you are used to living off of your base salary, then you won’t even notice the difference!

Related retirement savings challenges to Acquire Then Retire include: DCA is the Way, 52 Week Money, Feeling Rothy, Roth Me Bro, You’re FIREd, F U Money, Nomad No Problem, FIREd Up.

Benefits of the Acquire Then Retire Challenge

There are many benefits from completing the Acquire The Retire Retirement Savings Challenge. Why not treat your older self?

Building Your Retirement Savings

Saving money for retirement isn’t always easy. It can be tough to manage your immediate wants and needs while also thinking about your long-term future. By consistently bumping up your retirement contributions you’ll start to see your nest egg grow and compound interest take effect without sacrificing your short-term quality of life.

Compounding

By saving more for retirement now, you’ll increase the amount of time your money has to work for you. The beauty of compounding is that it can turn a modest amount of savings into a very large amount of money given enough time.

Feel More Secure

Running out of money in retirement is the number one fear as you approach retirement. Through the Acquire Then Retire Saving Challenge, you’ll become more confident that you will one day be able to retire and not have to worry about running out of money.

Conclusion

Worrying about running out of money in retirement is avoidable when you implement the Acquire Then Retire retirement savings challenge. Acquire Then Retire is a painless way that when implemented earlier in your life can capture the power of compounding interest. Regardless, get started today on the Ostrich App so you can live worry free and without sacrificing your quality of life.