Built for Small Credit Unions

Credit unions were built on relationships. We help you extend them into the digital world.

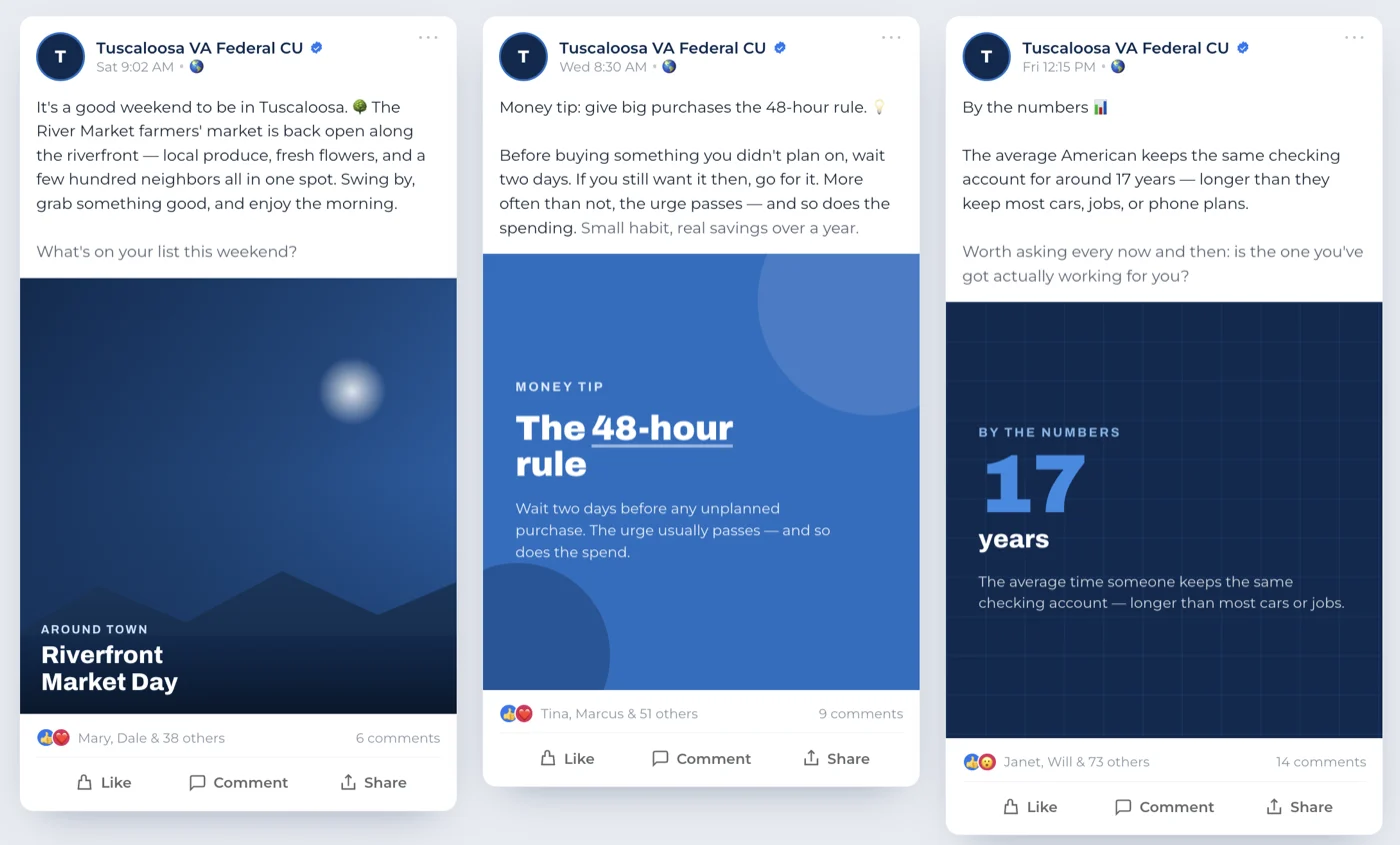

Your members don't come into the branch like they used to. But the relationship doesn't have to fade. Ostrich runs the digital side for small credit unions, especially those without a dedicated marketing team. That frees your team to do the work that only happens in person.

Let's talk about your members

Built for credit unions.

Trusted by the people who run them.